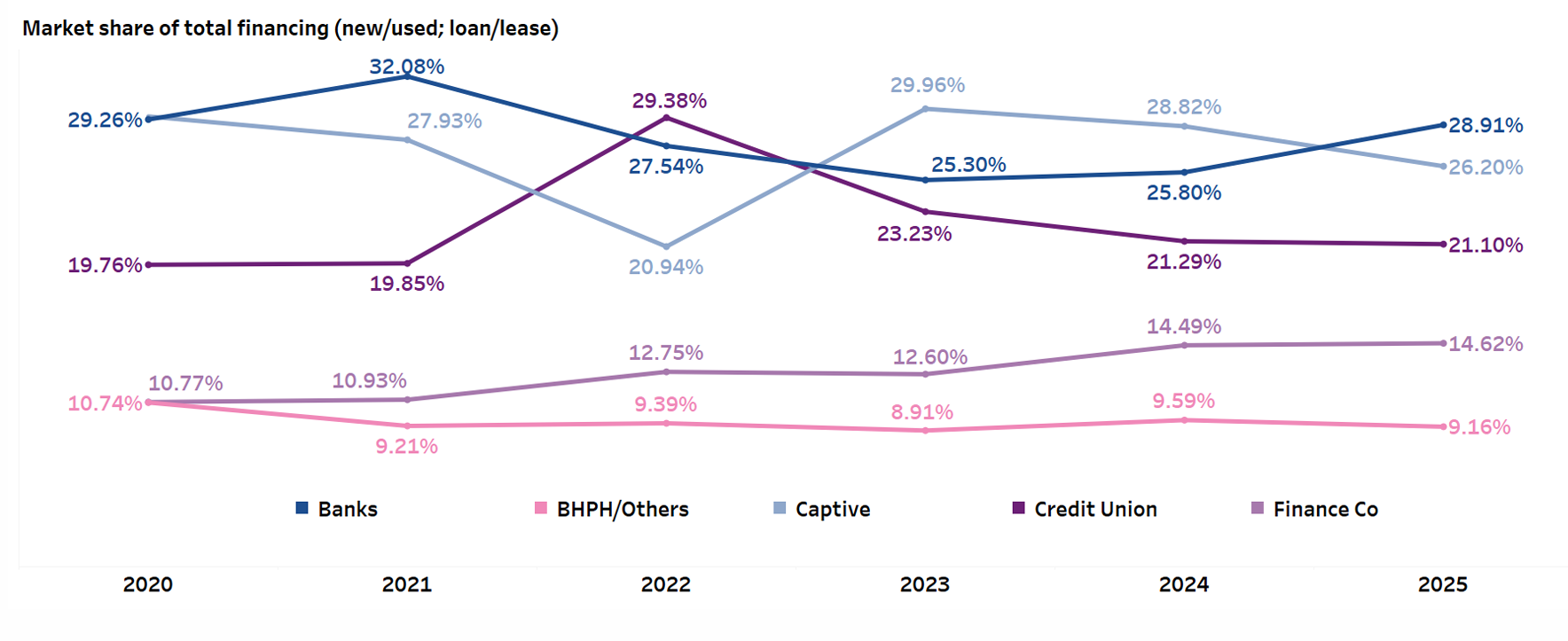

Amid a pullback in captive-led incentives and newly established relationships with manufacturers, banks saw the largest market share growth for total vehicle financing of all lender types in the third quarter.

Banks represented 28.9% of total auto financing across new and used, loan and lease in Q3, up 310 basis points (bps) year over year, according to Experian’s Q3 State of the Automotive Finance Market report. By comparison, captive share fell 262 bps YoY to 26.2%, while finance company share inched up.

Banks are looking to grow, with some opening their buy boxes or decreasing their minimum credit scores to tap the near prime or high-end subprime credit tiers, Melinda Zabritski, head of automotive financial insights at Experian, told Auto Finance News.

“Banks tend to be more prime, but at the same time, we are having that finance company growth, which is a bit more subprime — the two areas of the spectrum that are growing are the top and the bottom end,” she said. Banks are also “looking to buy a little older and help support those consumers who need to buy older vehicles to keep that payment down.”

Auto lenders are navigating a “complex” market benefiting from low unemployment and relatively strong consumer confidence but also navigating inflation, which is particularly challenging for lower-income borrowers, Sanjiv Yajnik, president of financial services at Capital One, told AFN.

“Cars have become way more expensive, and there are certain parts of our economy where salaries have not kept pace.” — Sanjiv Yajnik, Capital One

Credit union share was nearly flat YoY, according to Experian.

Despite cost pressures facing consumers, including higher expenses for vehicles, insurance and groceries, 2025 and 2026 are times of “cautious optimism” for financiers, Daniel Chiappone, chief lending officer at Melbourne, Fla.-based Space Coast Credit Union, told AFN at the end of November.

“Consumer demand will probably remain measured, but if rates ease … we can have a more predictable and supportive environment for auto lending,” he said. “We’ll keep a close eye on unemployment; it’s still low historically. As long as people need to work, they’ll hopefully finance their car.”

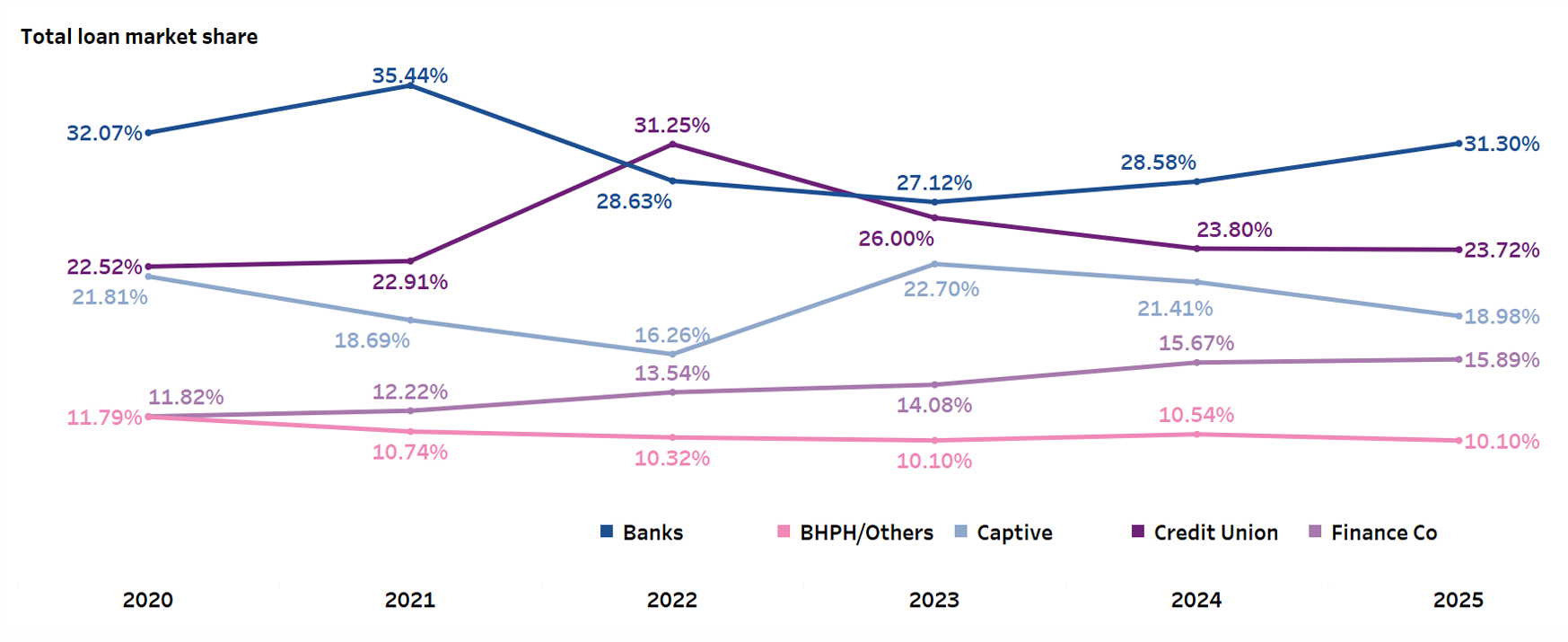

Bank loan share surpasses 30%

Banks also led the market for auto loan share at 31.3%, up 272 bps YoY, while finance companies also posted growth and other lender types lost loan share, according to Experian.

Some of the growth in bank market share can be attributed to Wells Fargo’s deal with Volkswagen, Zabritski said.

Wells Fargo in May was named the preferred lender for Volkswagen and Audi brands in the United States, with Ducati coming on in 2026. On the heels of the arrangement, Wells Fargo Auto’s originations in Q3 jumped 114.6% YoY to $8.8 billion.

“It won’t account for all of that share growth because of the market share of VW and Audi, but that’s going to account for some of it,” Zabritski said. “Also, Chase picking up more of the Tesla business.”

Chase Auto is one of Tesla’s preferred lenders. The bank also has private-label financing arrangements with manufacturers such as Subaru, Jaguar Land Rover, Maserati, Aston Martin and McLaren.

Banks also in Q3 saw about a 21% YoY increase in auto finance volume tied to borrowers with credit scores of 600 to 620, Zabritski said, noting that the data is for vehicles no more than 8 model years old.

“They were the only lending segment that grew the 620 and below volume,” she said. “That speaks to growth in subprime and accounting for the bank share increase as well.”

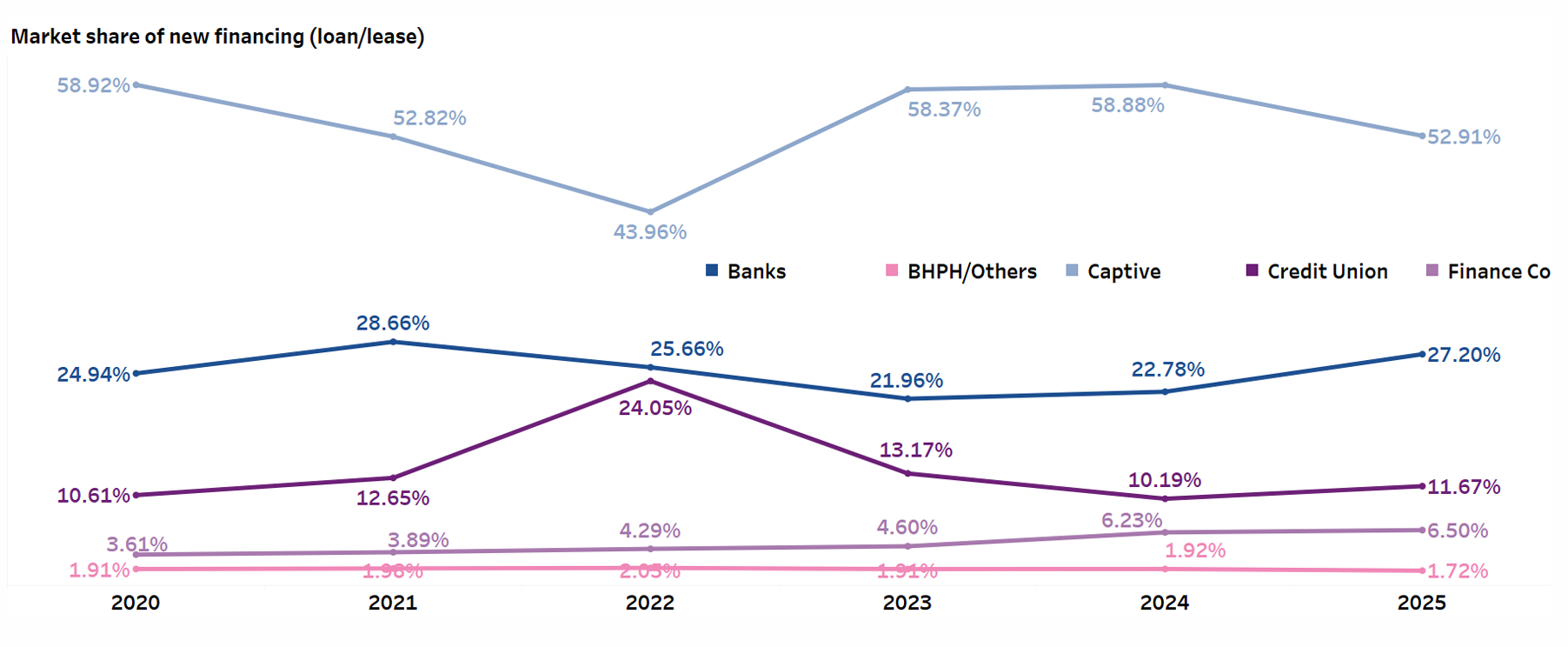

Captives lead new

For new vehicle loans and leases, captives continued to lead the market in Q3 with a 52.9% share, down from 58.9% a year ago, according to Experian. Banks were second at 27.2%, up from 22.8% a year prior, followed by credit unions at 11.7%, up from 10.2% in Q3 2024.

Amid competition, Indian Land, S.C.-based Sharonview Federal Credit Union is strategic about interest rates and portfolio growth, Kelton Graham, vice president of lending and sales, told AFN.

“We’re intentional with our interest rate selection,” he said, noting that rates vary between applicants who apply with the credit union and those who apply through dealerships. “Our direct members have a substantial market advantage. We’ve been told in the marketplace our rates are lower than what they’ve seen.”

As of Dec. 1, Sharonview was advertising auto loans with APRs as low as 3.74%. Sharonview’s auto origination volume year to date through Nov. 30 totaled $116 million, compared with $47 million a year prior, Graham said. The portfolio sat at about $200 million at the end of November.

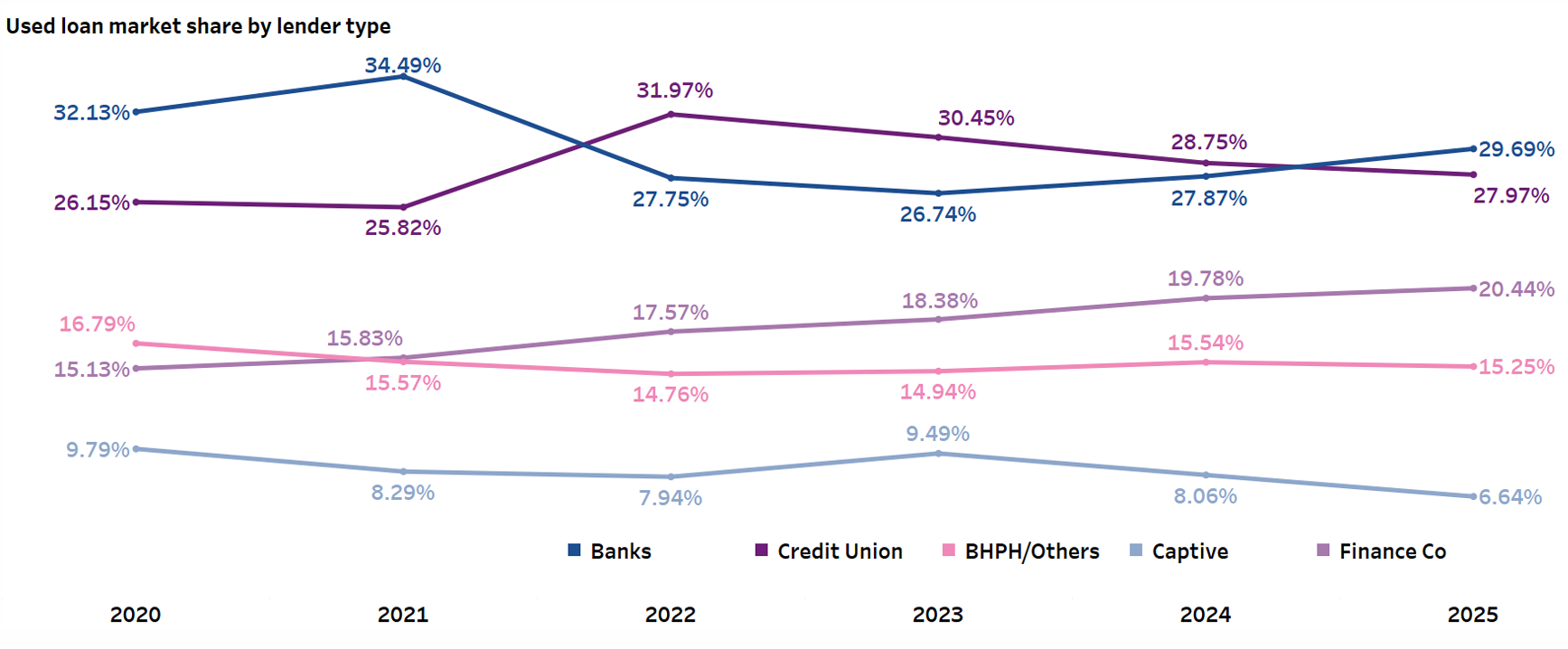

Banks lead used market, CUs follow

While banks led used-vehicle financing in Q3, they were closely followed by credit unions. Bank share grew 182 bps YoY to 29.7% while credit union share landed at 28%, down 78 bps YoY, according to Experian.

“On the used-vehicle side, we’ve seen demand consistent in our marketplace in the Carolinas,” Sharon View’s Graham said. “Certified pre-owned [cars] have played a part in that. Also, the price of new [vehicles] and the concern of tariffs have driven some demand to the used-vehicle side, but we’re also seeing inventory be a challenge.”

Banks and other lenders are also starting to finance older vehicles as affordability pressures mount, he said. “That’s going to be something key to watch in 2026.”