It’s dark outside and you are browsing available vehicles in your area from your phone as you plan your next purchase.

Though it’s after hours, the dealership agent has answered all your questions, given information on how to qualify for financing, helped you find the vehicle you’d like to purchase, provided an estimated monthly payment and scheduled a test drive at your local dealership.

The twist? You never left your couch or put down your phone, and the agent is AI.

As lenders adopt AI capabilities, virtual assistants have become more adaptive, responsive and human-like.

Gone are the days of canned responses. Generative AI-based chatbots now have personas and names — think Bank of America’s Erica, Carvana’s Sebastian and Capital One’s Eno, to name a few. The tech allows consumers to interact with lenders at all hours, improving their experience and cutting down on the need for phone calls to solve problems.

Building on that technology, some financial institutions are moving toward using AI agents that can make decisions with zero human intervention by pulling from available data.

“Agentic AI is going to be one of the most powerful tools that is going to be used across financial services.” — Sanjiv Yajnik, Capital One

“Agentic AI is going to be one of the most powerful tools that is going to be used across financial services,” Sanjiv Yajnik, president of financial services at Capital One, told Auto Finance News. “But to get there, it’s not a question of taking it off the shelf and using it; it’s a combination of many things. Each [AI agent] has to be built upon the use case.”

Agentic AI: The next iteration

Agentic AI is defined as the use of AI systems “capable of autonomous decision-making and actions,” according to a January report published by Citigroup.

By comparison, gen AI is a subset of AI that uses patterns learned from data to create new content, including text, images and code, according to Citi. AI describes computer systems and tech that can “stimulate human intelligence” and perform automation and analysis. As institutions build and train their models, the type of AI they use becomes more sophisticated.

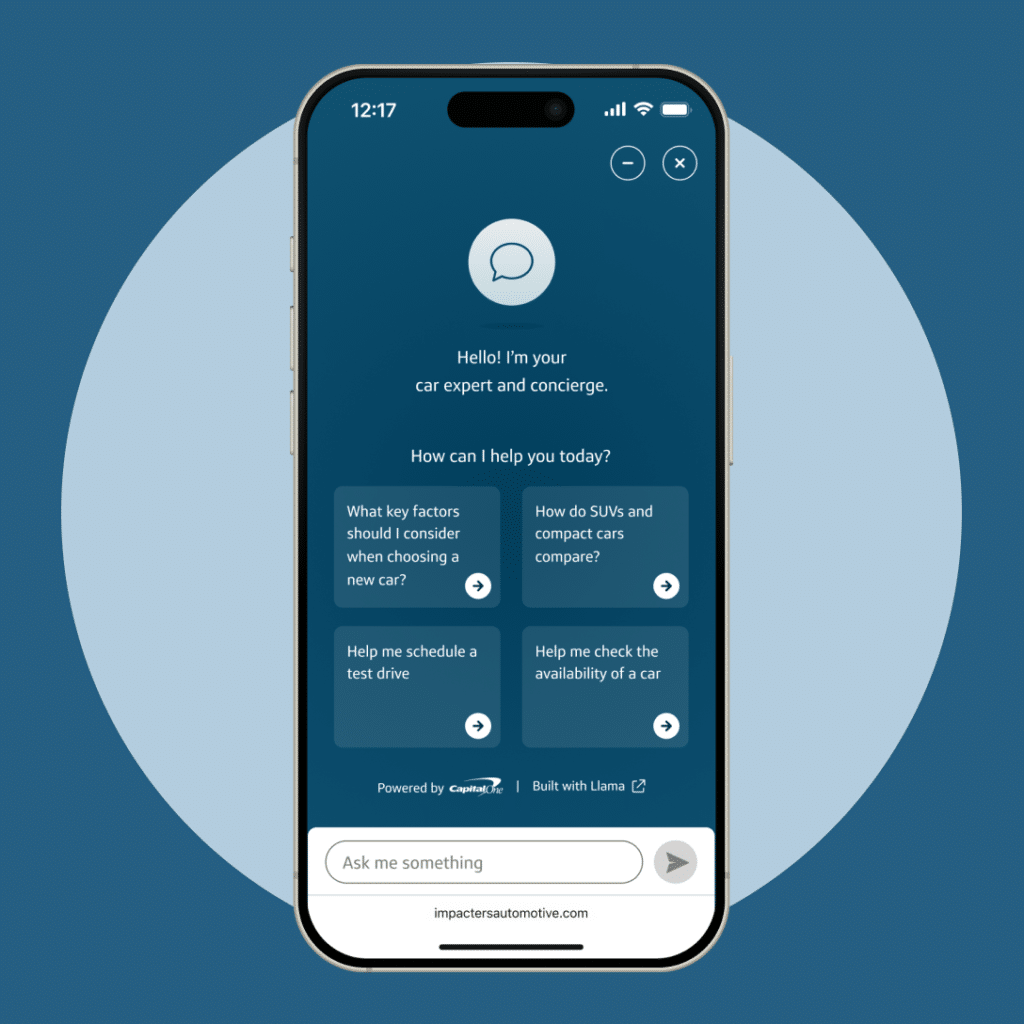

Capital One’s new agentic AI tool, Chat Concierge, can answer consumer questions, provide vehicle comparisons and financing options, and schedule a test drive — all during a single online transaction.

The tool builds upon the bank’s gen AI-based tech stack along with external large language models and open-source technology, and uses Capital One’s proprietary data, Yajnik said.

“Agentic AI is a very sophisticated tool. Instead of having one agent trying to answer all the questions, you get expert AI tools,” Yajnik said. “Each one is an expert in a particular domain, and then you get them to talk to each other. … It can connect with the person in a more human-like way.”

AI agents have “conversations” to get the information needed or complete tasks, Yajnik said.

“For instance, if a customer wants to schedule an appointment … the scheduling AI will have to talk back to the other agentic AI to say, ‘Please get me this information’ and it will talk to the customer,” he said. “It’s a pretty involved, complex thing. You need a tremendous amount of data.”

Capital One’s auto portfolio rose 3.7% year over year to $76.8 billion in the fourth quarter as full-year originations jumped 28% YoY to $34.5 billion.

AI-assisted solutions

Agentic AI is not replacing employees or taking over tasks — in its current form, Amitay Kalmar, chief executive of AI-powered auto lender Lendbuzz, told AFN. Instead, the emerging tech is mainly being used to assist employees in backend operations and boost productivity.

“The maturity of [agentic AI] is not there yet to replace humans in most roles,” Kalmar said.

“The maturity of [agentic AI] is not there yet to replace humans in most roles.” — Amitay Kalmar, Lendbuzz.

Boston-based Lendbuzz is exploring how agentic AI can assist with tasks related to customer service and language translation, he said.

The customer service front includes “any written communication coming into or [leaving] Lendbuzz, whether it’s via chat or email,” Kalmar said, noting that in this case, agentic AI can offer shorter response times.

“If you’re able to have an AI agent create or polish a draft that goes out then, instead of replying to 10 messages an hour, [the agent] can reply to 50 messages an hour,” Kalmar said. “It’s not replacing the [employee], but it’s significantly increasing productivity by assisting the [employee] with drafting and replying to messages.”

Backing this up, more than 60% of respondents to a survey by AI leader Nvidia named customer experience and engagement a top use case for gen AI at their companies. The survey polled 600 global financial services professionals, according to the report “State of AI in Financial Services: 2025 Trends.”

Nvidia projects agentic AI will be the next development in gen AI for tasks across customer service, cybersecurity and investment analysis, according to the report.

Other use cases for agentic AI in auto finance, according to digital document company Lightico, include:

- Underwriting and risk management;

- Fraud detection; and

- Collections and servicing.

Assistance at all hours

The assisted use cases don’t stop there. Dallas-based fintech Yendo is using agentic AI to handle requests overnight, CEO and co-founder Jordan Miller said.

“We’ll have dozens of people sign-up between 3 a.m. and 4 a.m., and obviously there’s no one working to answer their questions, but the AI agent is there,” he said, adding that Yendo built and operates about 60 AI agents.

“We’ll have dozens of people sign-up between 3 a.m. and 4 a.m., and obviously there’s no one working to answer their questions, but the AI agent is there.” — Jordan Miller, Yendo

Yendo also uses in-house models for its AI chatbot and AI agent loan servicing provider Salient to perform collection calls, Miller said. Through Salient, “the AI agent can take payments over the phone, and the cost of these AI systems are typically 90% [less expensive] than a human-based one, with better results,” he said.

Yendo views AI “as a force multiplier of smart people,” Miller said, and has implemented the tech in other internal operations, including fraud detection models and verification tools.

Meanwhile, AI is also assisting Lendbuzz with its language and translation services, Kalmar said. “Our customers speak a wide range of languages, and it’s very hard to hire [human] agents that speak all these languages,” he said. “You now have an agent that’s enabled with technology to provide better service, so the consumers overall are going to benefit.”

As of Sept. 30, 2024, Lendbuzz’s serviced portfolio stood at $2.1 billion, originating $398 million in Q3 2024 loans, up 29% YoY.

Building on Gen AI

Agentic AI was born out of the natural evolution of AI technology, from perception AI that includes speech recognition and medical imaging, to gen AI content creation and digital marketing, to agentic AI and eventually physical AI such as self-driving cars, Capital One’s Yajnik said, citing information shared by Nvidia CEO Jensen Huang during a recent presentation.

“The innovation in gen AI is continuing at a breathtaking speed,” Yajnik said. “There’s a lot of focus right now on the basic underlying models. … Agentic AI is the next step in the evolution of AI. It’s the future because it allows one to be much more human-like in the answers and the connections with customers.”

“The innovation in gen AI is continuing at a breathtaking speed. Agentic AI is the next step in the evolution of AI.” — Sanjiv Yajnik, Capital One

This evolution of AI symbolizes a ladder of potential — one some lenders are willing to climb faster than others.

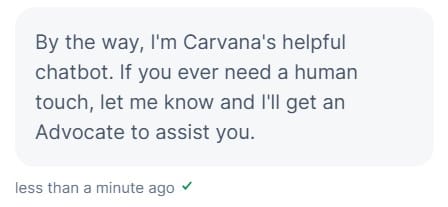

At Carvana, for example, one of the first rungs on its tech ladder was the chatbot Sebastian. While Sebastian may seem like a simple chatbot, the application represents “the brain that [Carvana is] building,” CEO Ernie Garcia said on the retailer’s Feb. 19 earnings call.

Sebastian, launched in late 2018, began as a chatbot capable of “canned responses” but has evolved to be more adaptive through a series of iterations and trainings, Matt Dundas, vice president of finance at Carvana, told AFN.

“We’re able to train on internal materials in a way where these models can learn more organically, versus having to anticipate all the different questions and have canned responses,” he said.

(Video/Auto Finance News)

Gradual improvements to the model contributed to a 20% YoY reduction in average calls per purchase in Q4 2024, while the percentage of Carvana customers who interact exclusively with AI-powered chat tools nearly tripled during the past two years, Dundas said.

“In terms of the quality of customer experience, in many ways it’s better because [consumers] can get 24/7 support.” — Matt Dundas, Carvana

“A big part of that [reduction] is from AI technology and Sebastian being able to handle more calls without having to involve human agents,” he said. “In terms of the quality of customer experience, in many ways it’s better because [consumers] can get 24/7 support and the response times are virtually instant.”

Carvana’s full-year originations came in at $8.3 billion in 2024, up 37.9% YoY.

Evolving tech drives market competition

Unsurprisingly, the evolution of AI adds a new layer to how lenders and fintechs compete for consumers, Garrett Laird, director of decision science with Chicago-based fintech Amount, told AFN.

For fintechs, AI and machine learning offer a wealth of additional resources, data and tools needed to compete against more established, traditional lender types, Laird said.

“When you’re a digital lender with no brand awareness and you’re competing on affiliate channels like Credit Karma and Lending Tree, you have to be precise in the way you’re making credit offers and pricing decisions,” Laird said. “For any one decision, there are four-plus models being run to evaluate the risk of a consumer, from fraud and identity to credit to bankruptcy risks,” he said.

The rise of AI has fueled a shift in market competition, Laird said.

“A lot of the fintechs owned and dominated that [digital] space, and now more traditional lenders [such as] banks and credit unions are starting to realize the value there,” he said. “That’s had a big impact in the way lenders are thinking about underwriting.”

“Fintechs have flipped the script.” — Shraddha Mehta, SFS

“Fintechs have flipped the script,” according to Shraddha Mehta, senior data scientist with Stellantis Financial Services (SFS).

Previously, “banks and credit unions dominated auto lending, and getting approved for a loan meant piles of paperwork, in-person visits and waiting days for a decision,” she said, noting that loan approvals were mainly based on credit scores, which left many buyers with limited options.

But now?

Tech-forward lenders like Carvana, Upstart and AutoFi are giving control to the consumers through added tools like pre-qualification services, while also opening financing to more consumers by tapping into alternative data like utility payments and rental history, Mehta said.

Training the models

Upstart’s AI-driven lending platform uses predictive AI to measure a borrower’s risk of default and offer lower rates to consumers, Alex Rouse, vice president and general manager of auto, told AFN.

“We continue to release new AI models, and those models get smarter as they get access to more data.” — Alex Rouse, Upstart

“We continue to release new AI models, and those models get smarter as they get access to more data and more loans and when we release features that make them smarter,” he said.

“One of the features that we released in a recent model is that we estimate the value of a vehicle at repossession at the time of pricing,” he said, noting data fed to the model includes geographic, borrower and vehicle information. “[We’re] able to make a more accurate prediction. That means it’s going to provide more accurate, lower rates for consumers.”

Meanwhile, Carvana and its servicing partner Bridgecrest are experimenting with agentic AI integrations to offer a more approachable solution for consumers needing to chat about sensitive subject matter such as payment plans or financial struggles, Dundas said.

“Customers want to interact in the digital space, and it’s awkward discussing due balances and hardships on the phone,” he said. “Agentic AI technology is well positioned to handle those conversations and offer payment plan options and extensions without somebody having to get on the phone and awkwardly negotiate back and forth.”

“From streamlining processes to improving risk assessment and personalizing customer experiences, AI is changing the game.” — Shraddha Mehta, SFS

SFS’ Mehta added, “From streamlining processes to improving risk assessment and personalizing customer experiences, AI is changing the game in ways that were unthinkable just a few years ago.”

Addressing barriers

Even with an abundance of use cases and success stories, uncertainty and caution have emerged regarding AI, Amount’s Laird said.

“There’s a lot of uncertainty around regulation, and the [Consumer Financial Protection Bureau] and its existence or nonexistence,” he said. Traditional banks, for example, are “apprehensive about AI use cases like an agent talking to their customers or guiding them through anything.”

“The fintech players that are more comfortable with [AI] might be the ones pushing those boundaries,” Laird said. “If they’re able to start doing it and aren’t slapped down by the CFPB or other regulatory bodies, then that opens the door for more traditional financial institutions to follow suit.”

Other concerns include the lack of “explainability” that often comes with new iterations of AI in the industry, Laird explained.

“One reason why there is some hesitancy and pushback using generative AI and large language models is the lack of transparency on how those decisions are reached,” Laird said. “For any lending decision that we make, including marketing, you have to be able to justify why Customer A was offered something and Customer B was not.”

“For any lending decision that we make, including marketing, you have to be able to justify why Customer A was offered something and Customer B was not.” — Garrett Laird, Amount

The issue remains that the higher you climb the ladder of AI iterations and large language models, the harder it is to explain how models reached their answers due to their “black box nature,” Laird said. This refers to transparency challenges surrounding new AI systems given that responses are typically provided based on inputs and outputs without much explanation or reasoning.

Curating transparency, successful AI

The key to building out agentic AI, Capital One’s Yajnik said, is to:

- Ensure the data feeding AI models and agents is clean;

- The ways the models are trained are sound and;

- The AI can communicate with consumers in an acceptable and believable tone,

People building the architecture must also understand how consumers will use the technology, he said.

Agentic AI “cannot be built by throwing things over the fence,” Yajnik said. And to his point, checks and balances are needed to address AI hallucinations, or instances in which an AI model generates answers or outputs that are misleading, incorrect or fabricated.

“Sometimes tools can give confident information that may be wrong,” he said. “The more sophisticated a system becomes, the more it learns. The more you train it, the less of these hallucination issues that you have.”

SFS’ Mehta stressed similar best practices, saying, “While AI offers significant advantages, these benefits only come to life when applied correctly and in the right context.”

She added that the “true value” of these evolving technologies lies in “thoughtful application,” which requires lenders to:

- Understand the cost-benefit balance;

- Align AI initiatives with specific business requirements; and

- Have the right expertise.

“When applied to the right problems, AI can deliver incredible results,” Mehta said. “However, without careful consideration, it can quickly turn into a money pit, especially if the need for AI is not well-defined or if it’s implemented without a clear understanding of the business problem.”

‘Full-scale transformation’ in progress

Years from now, the financial services industry will be digging deeper into the latest tech advancements and use cases, placing agentic AI at a lower rung on the ladder of capabilities. For now, though, agentic AI symbolizes the industry’s evolving potential and a heightened focus on meshing tech capabilities with human-like connections.

Last year alone, 37% of venture capital funding went to AI-based startups, a number expected to climb in 2025, according to the Citi report.

“By providing innovative solutions across areas like loan processing, risk assessment, compliance, fraud prevention and customer service, fintechs are playing a crucial role in modernizing financial infrastructure,” Mehta said.

Citi identified financial services as the “second-largest consumer of gen AI after the telecom and media sector” and noted agentic AI is in an “experimental phase.” However, references to agentic AI from tech giants in corporate documents and press articles increased by 17 times in 2024, according to Citi.

“The integration of AI and machine learning into auto finance is far from just an incremental improvement. It’s a full-scale transformation.” — Shraddha Mehta, SFS

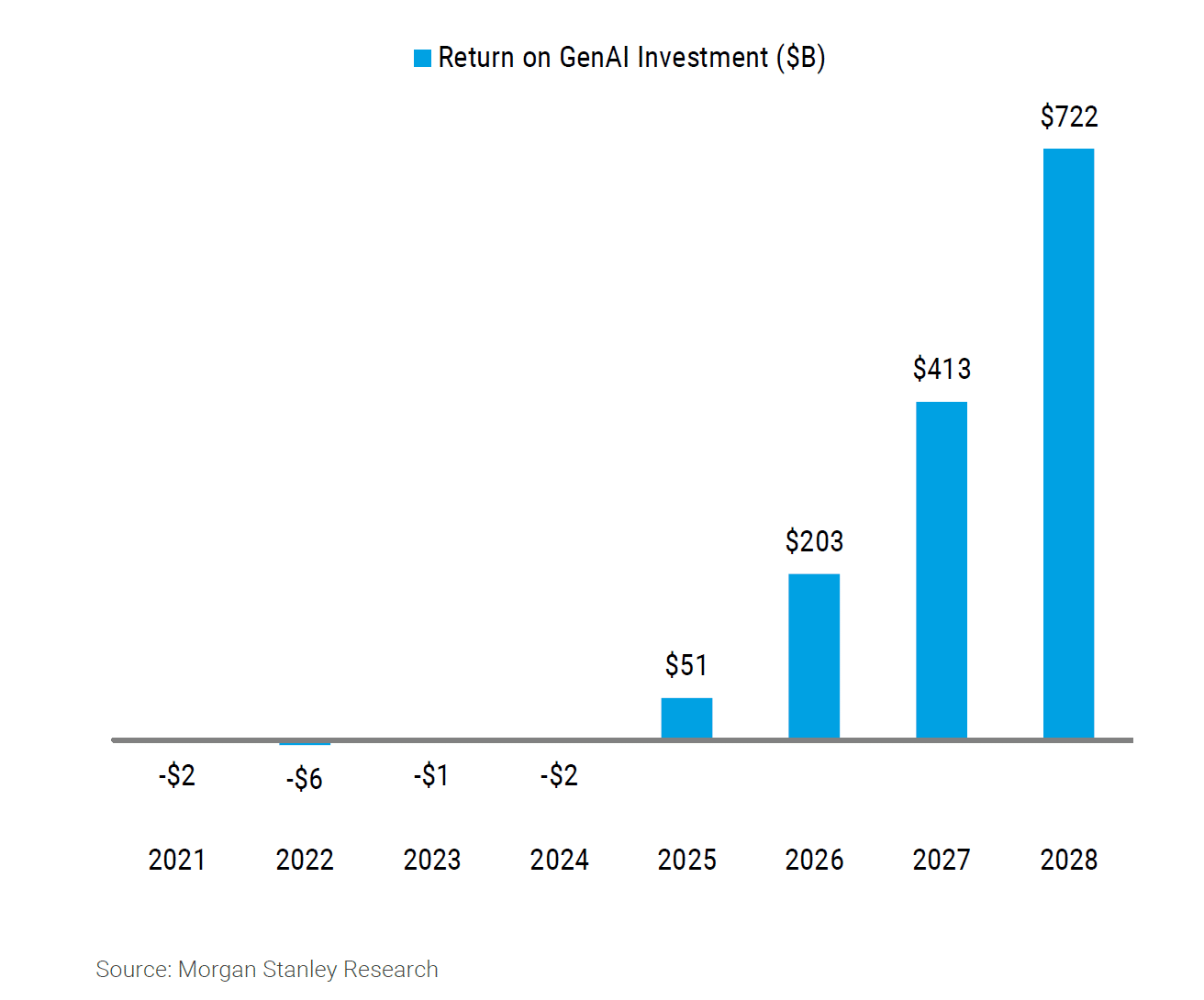

The coming years are also likely to bring notably higher returns on investment in AI, according to Morgan Stanley research.

In fact, companies’ return on investment in gen AI is projected to rise to $722 billion by 2028 compared with $51 billion in 2025 and $203 billion in 2026, according to Morgan Stanley.

“The integration of AI and machine learning into auto finance is far from just an incremental improvement. It’s a full-scale transformation,” SFS’ Mehta said. “As these technologies continue to evolve, we’re only scratching the surface of what’s possible.”

Auto Finance Summit East 2025 is set for May 12-14 at the JW Marriott Nashville featuring fireside chats with Santander Consumer USA and Chase Auto. Visit autofinance.live for more information. Early-bird registration is available here.